Why Life Insurance Interest is High in 2023

Last Updated on September 6, 2023 by bail_admin

Here’s a hard truth: life insurance interest is high in 2023.

A lot of folks think that just having a policy is enough. They say, “If I have coverage, my family will be protected”.

If only it were that simple…

To truly benefit from the surge in life insurance interest this year, you need to understand what’s driving this trend and how it impacts both consumers and industry professionals.

Research shows, there are significant factors at play influencing consumer behavior.

Let’s explore the causes behind this topic in-depth.

Life Insurance Interest in 2023: A New High

The year 2023 witnessed a significant surge in life insurance interest, particularly among the younger generations. This is not mere speculation; there is concrete data to support this trend.

A Look at the Numbers

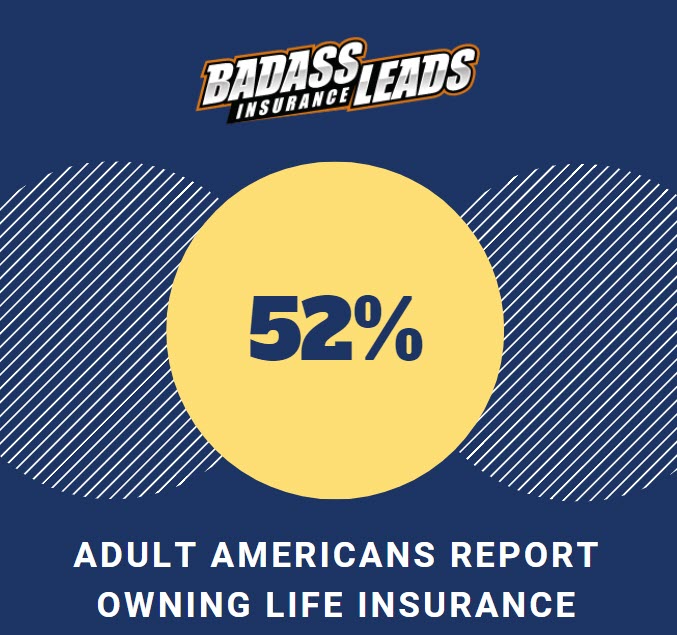

52% of Americans report owning life insurance.

Around 39% of consumers have expressed their intention to purchase life insurance within the next year. However, a closer analysis reveals that Gen Z and millennial adults are the driving force behind this trend. In fact, an impressive 44% of Gen Z adults are planning to buy life insurance.

Millennials Lead The Charge

As we move further down the age spectrum, the interest in life insurance among millennials has reached record highs, with a staggering 50% of all millennials planning to get insured in the near future.

This shift is not without reason. With an increasing emphasis on financial literacy and a growing awareness of future security amidst global uncertainties, millennials are taking proactive steps to secure their financial futures like never before.

The Changing Face Of Policyholders

In previous years, older individuals were typically seen as the typical policyholders. However, recent trends indicate a noticeable shift towards younger demographics purchasing insurance policies.

Economic Stability & Financial Planning

Today’s youth understand the value of securing their financial futures early through mechanisms like insurance plans. Youth are knowledgeable and aware of what they need to do for their own benefit.

Rising Health Concerns & Uncertainties

Ongoing global health crises have underscored the importance of having robust protective measures, such as adequate health coverage, including term-life insurance.

Maturity Benefits And Long-Term Savings

In addition to protection against unforeseen circumstances, many modern-day policies offer attractive maturity benefits that serve as long-term savings tools, making them appealing options for those seeking wealth creation alongside safeguarding their interests.

Huge Opportunities For Agents And Brokers

There’s a huge wave of interest coming from the younger crowd. This opens up amazing chances for agents and brokers working with aged leads.

Unmasking The Coverage Gap and Its Impact

There’s a lurking beast in the financial world, and it goes by the name of “life insurance coverage gap”. Sounds ominous, right? Well, it is. This term refers to those individuals who either have zero life insurance or simply don’t have enough.

The repercussions aren’t just personal; they ripple outwards, impacting families and dependents as well. Let’s delve into this further.

Digging Into Life Insurance Ownership Stats

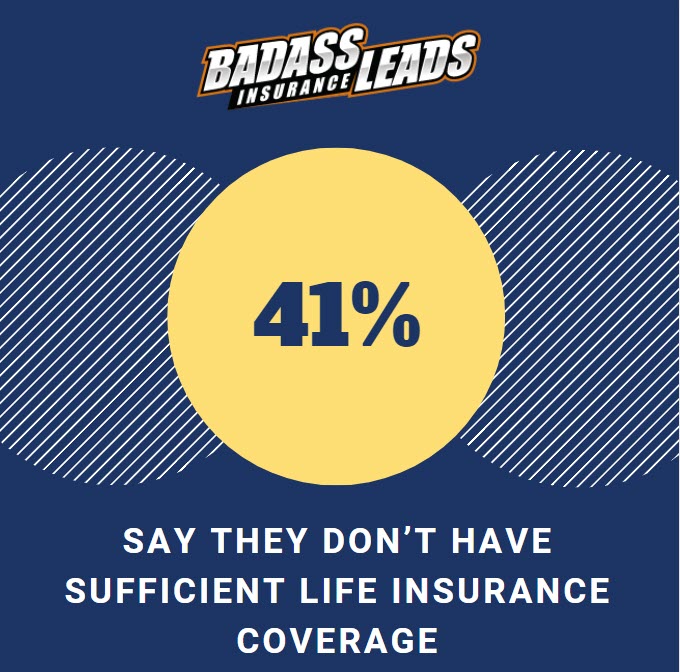

A staggering 41% of adults feel their life insurance coverage would be insufficient if tragedy were to strike, with Gen Zs only having a 40% ownership rate. That means nearly half of us are walking around with this coverage gap hanging over our heads.

If we zoom in on Gen Z adults (those young whippersnappers), only 40% own any form of life insurance policy. Sure, being younger often means having fewer responsibilities, but these numbers still ring alarm bells.

The Single Mothers’ Predicament

We can’t discuss insufficient life insurance coverage without mentioning single mothers – an already vulnerable group that’s even more at risk here. Only 41% of single mothers have some sort of policy protecting them. (National Association Of Insurance Commissioners)

This isn’t good news because when you’re solely responsible for your kids’ well-being today and their future tomorrow… well, having no backup plan puts them squarely in harm’s way should anything happen to mom.

Bridging The Coverage Gap: It’s Time To Step Up

We’ve laid bare the stark reality above, so now let’s turn this ship around. We need all hands on deck from across industries to encourage consumers to take control. .(Financial Planning Association)

So, to make the right choices about picking plans that match their unique needs and lifestyles, folks from all walks of life need to arm themselves with knowledge. It’s all about finding what fits best for you in today’s diverse society.(Financial Planning Association)

The Higher Need for Life Insurance Among Single Mothers and Young Parents

When it comes to life insurance, single mothers and young parents are the groups that feel a stronger pull towards this safety net. Why? Let’s delve deeper.

Understanding Single Mothers’ Need for Life Insurance

Pivot Point #1: Financial Responsibility in Solo Mode

Single moms carry the financial weight of their families on their shoulders. It’s a one-woman show where 41% have stepped up with life insurance policies. But what about the rest?

A Stark Reality:

An alarming 59% of solo mamas agree they need more coverage, spotlighting an unsettling truth – many households teeter on the brink of economic hardship if tragedy strikes unexpectedly.

The Great Divide:

This awareness points to a chasm between recognizing life insurance importance and actually having enough coverages in place due to hurdles like affordability or understanding policy intricacies.

Tackling The Issue Head-On:

We need comprehensive education around policy benefits, along with affordable plans tailored specifically for these superheroes without capes – because let’s face it, being a single mom is no easy feat. Proper coverage can offer peace knowing children will be financially secure even when she’s not there anymore.

Why Young Parents Feel Underinsured

New Generation Challenges:

Young parents today span Gen Zs and millennials who confront unique obstacles ensuring long-term security for themselves offspring. Averagely, 56% feels underinsured suggesting recognition significance but grappling obtaining sufficient due various barriers like cost complexity involved choosing suitable policies;

Current Coverage Gaps:

Research reveals that while general population rates stand at 52%, parents minor children more likely (59%) own some form life insurance. However feeling inadequately insured highlights gaps within current provisions which may leave families exposed during unexpected events. Here’s why:

- Just Scratching the Surface: Although most youngsters have a bit of understanding, they’re not quite deep into it yet.

Cracking the Code: Demystifying Life Insurance Purchase

The quest for life insurance can feel like a puzzle, especially when you’re unsure about the right types and amounts for you. Beneath the surface of confusion lies an answer; let’s uncover it.

Here’s how we can turn this mystery into an open book:

Misunderstanding Types And Amounts Of Coverage

Only about one-third (33%) of younger generations feel they understand life insurance well enough to make informed decisions. This creates a significant knowledge gap in buying policies that needs to be addressed promptly.

You may be wondering about term versus whole life insurance or even if there are plans with investment options like universal or variable insurances. We understand that it’s complex stuff.

Tackling The Knowledge Gap Head-On

We need to confront these knowledge gaps head-on by making education our secret weapon. Explaining how different types work, factors that affect cost, and offering guidelines on coverage based on individual circumstances could help bridge this chasm.

A great place to start is Investopedia’s guide on Life Insurance Basics. It gives anyone interested in understanding various policy options available today a leg-up.

Busting Myths About Expenses

Another stumbling block that people often trip over is misconceptions about expenses related to premium costs. They believe coverage will burn holes in their pockets without realizing they might be exaggerating those figures. So let’s bust some myths together because expense misconceptions shouldn’t stand between them and financial protection.

Unfortunately, many cite expense as a top reason for not getting covered, largely due to skewed perceptions rather than factual evidence. Insurers should shed more light on pricing structures – clarity goes hand-in-hand with confidence after all.

Understanding the perceived high cost of premiums requires us again – yes, you guessed it – education. A good read would be Insure.com debunking common Life Insurance Myths.

FAQs in Relation to Life insurance interest is High in 2023

What is the interest rate on a life insurance policy?

The interest rate varies, depending on your policy type. Whole and universal life policies may earn between 2% to 6%, but it’s contingent upon the insurer’s declared rates.

How many Americans have life insurance in 2023?

In 2023, approximately 52% of American adults own some form of life insurance coverage according to recent surveys.

How much a month is a $500,000 whole life insurance policy?

A $500k whole-life policy might cost around $300-$400 monthly for healthy individuals aged mid-30s. But prices swing widely based on age, health status, and lifestyle factors.

How much is $100000 in life insurance a month?

A healthy individual in their mid-30s could pay roughly $10-$20 per month for term-life coverage worth $100k. Rates fluctuate due to age, health condition, and other variables.

Visit Badass Insurance Leads, let’s help you ride this wave of high life insurance interest together! Make 2023 your year of exponential growth!